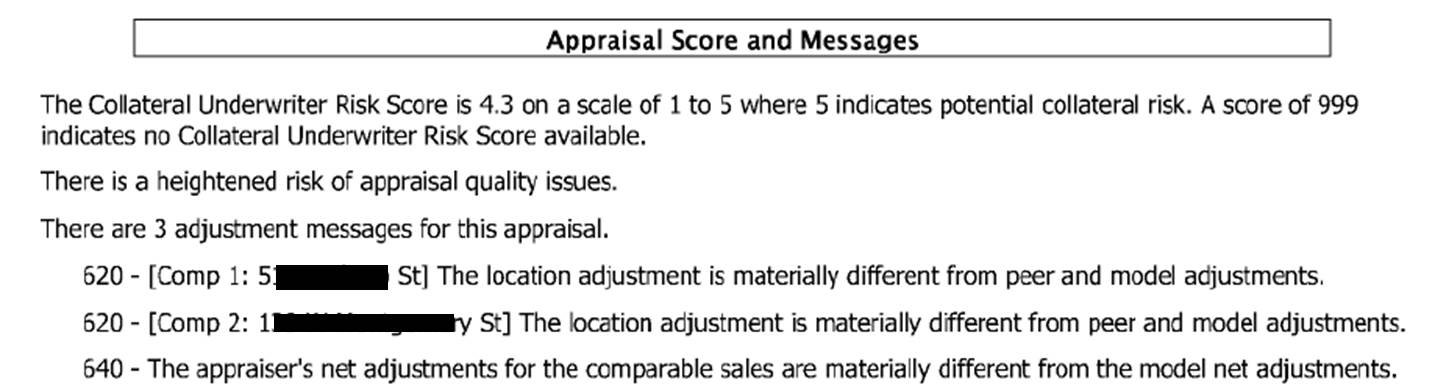

Collateral Underwriter Message

Return to Richard Hagar’s Story

Visit Working RE’s Collateral Underwriter Blog and leave a Comment

Return to Richard Hagar’s Story

Visit Working RE’s Collateral Underwriter Blog and leave a Comment

by D.A. Dipietro

I’ve seen quite a few articles stating: Appraisers need to raise their fees. Huh, the AMC’s have that set in stone. If we don’t like it, don’t do work for them. Not sure how all the composers of these news article(s) expect us to just “raise our fee”. I’m sure RELS, TSI, etc etc are going to go for that. Not!

-by John PA Appraiser

Very informed response from Michael!

-by Michael F. FOrd, CA AG

I absolutely agree. Personally I think the fees should be tied to federal pay scale equivalents. The feds civil service have already done the compensation and benefit package studies and determined ‘fair’ pay for appraisers. we merely need to convert it to reasonable approximations of how long each type of assignment takes start to finish.

-by Michael F. FOrd, CA AG

Richard, you cannot be serious! Yes, a USPAP compliant appraisal review IS a good thing, but that is not what’s being offered.

In the past, poor appraisal reviews were such a serious problem in the industry that USPAP was modified to set very specific MINIMUM standards governing criticism of a licensed professional appraisers work. Reputations and preserving the ability to earn a living were considered worthy of protecting.

NOT ONE of the CU messages you demonstrated here is worthy of an appraiser response. NOT ONE! While you fairly pointed out that the appraisal scenario that existed may have been completely different than that indicated by the CU data, the scenarios you DID address were ‘best case’ for the CU. NOTHING in the CU default comments indicate WHY an appraiser should second guess their work. A database is NOT MY PEER!

Richard, respectfully, why are you and so many others so willing to accept non USPAP complaint “review” of your work?

Form appraisals were originally designed for assignments not requiring fully self contained narrative analyses and reporting. Over time, the forms were modified to provide more and more data in hope FNMA could eventually learn how to encourage correspondents to make good loans.

The requirement for appraisers to include information and supportive data in narrative addenda grew and grew, though we KNOW that addenda information doesn’t even make it past the xml gate of the intended users.

So, we continue to provide USPAP compliant appraisals. Lenders and FNMA continue to circumvent our ability to comply with SR2 while themselves failing to comply with SR3!

OK. There is a “reasonable” cost for this. There is also one that is “Customary” for federally employed appraisers that routinely have to deal with bureaucratic incompetence.

From now on I expect all fees to be consistent with annualized income for federal civil service appraisers calculated as follows: Trainee = GS 7; Licensed residential appraiser from 3 to 5 years experience = GS 9. Residential Certified GS 11 to 12; General Certified with over 15 years GS 13 to GS 15 PLUS location adjustment for COLA (California is 27.16% of base); PLUS 3% of annual gross up to $100k for Thrift Savings (call it IRA equivalent) for FORTY hour work weeks with all federal holidays off; AND only 50 work weeks per year for those with less than 3 years experience and 3 weeks for those with more than 3 years experience; PLUS fed contribution to Social Security (7 1/2% of adjusted gross). Did I forget the mileage allowance of $0.505?

in California, a 3 year non certified appraiser doing NON COMPLEX work would have a salary equivalent of $53,915 including the 27.16% location allowance; +3% or $1,671 savings / IRA; plus SS contribution I’ll leave off for the time being.

The 3 years experience non certified appraiser expects compensation of $55,586 for a 50 week year of 40 hours per week (2,000 hours-holidays -48= 1,952). To PROPERLY complete each non complex assignment including highest and best use analysis and regression it is 10 to 12 hours work per report. Say 12. The appraiser can complete 3 1/3 per week start to finish. The number of adjusted weeks per year are 48.8. Extended this is 48.8 x 3.33 = 162.5 assignments per year.

The MINIMUM amount that the 3 year experienced appraiser should charge for non complex work is $342.07 per report (add $30-$35 for gas and social security equivalent comp).Step increases also kick it up a few thousand a year. (keep in mind that if they work for a certified appraiser that reviews their work something above this is required to compensate for that review).

The problem is that most assignments are no longer non complex in many markets. The fact that FNMA still has “conforming loan limits” well above norms indicates the truth of this. Complex market conditions exist throughout the nation. Additionally, many AMCs will not hire appraisers with less than 5 years experience and or residential certification. FHA requires residential certification.

THAT puts the base at (GS 11) $58,562 x 1.2716% = $74,467 + 3% = $76,701. The experienced appraiser is faster and more skilled but the work is more complex so that it still takes 10 to 12 hours on average per report for full USPAP compliance. $76,701 / 162.5 = $472 per report. MINIMUM plus another $30-$35 for mileage and social security = $502 to $537 for the NEW Residential Certified appraiser with only 5 years experience. The 5- 10 years or 15 to 20 years experienced certified appraiser will necessarily be much higher. (This is consistent with federal pay scale step increases within grade for longevity).

So far we have not addressed 2-4 unit income property. At a minimum its GS11 work; possibly Grade 12 ($70,192 x 1.2716% = $89,256 +3% = $88,844.

ON TOP of these minimal base professional LABOR fees are office expense (rent, phone, toner, high speed internet, fax machine, cell phone & land line, computer, multiple software platforms such as A La Mode, Click Forms, ACI, MS Word, Excel, Adobe reader AND writer, Drop Box. Plus local/regional mls fees. Plus CAR / NAR fees; PLUS data verification service fees (NDC alone can be $900 a month!; Real Quest, Realist, etc.), 1004MC software; Data Import software to auto populate (I don’t use these) Cameras, thumb drives, typists and or receptionist, etc..

At a minimum these are at least 25% of every single assignment. Multiply each pay grade per appraisal fee by 125%!

C&I rate swill necessarily be much higher annuals ranging to $100k to $120k+-

FNMA can keep falling for every new razzle dazzle software that comes down the pike claiming to ‘replace’ the reviewer; monitor the appraiser, prevent fraud, etc. but until REASONABLE minimum fees are established necessary work will continue to be short cut. Unlicensed appraisers will continue to support the dishonest appraisers working for impossibly low fees, and those that remain honest and of high integrity will continue to be starved out of the profession.

Join your state coalition and more importantly, your national American Guild of Appraisers where we can fight together to improve out lot rather than merely ‘accepting it and going forward’ under non professionals criteria.

-by John

My opinion is that Fannie is creating more problems. The Articular – “Collateral Underwriter: First Feedback” is also INCORRECT when it assumes that “We tried the path of banks not questioning appraisals and look where it got us…$7.2 trillion in economic harm”. ****TOTALY WRONG**** Its Comments Like This That Misleads Everyone To The Real Facts. Try President Clinton changing the banking laws “to expand mortgage loans among low and moderate income people” (New York Times, September 30, 1999). The Government caused the entire problem of the past 10 years. I believe Fannie gets all their Data (Comparables) from appraisals and determines acceptable adjustments from Data (Comparables) from appraisals they receive. If “Fannie’s CU takes over the appraisal process with the only inspection needed will be by an inspector for $50” – Fannie will run out of current Data (Comparables) in three to six month. The real problem is Government Gone Wild!

-by Gary Crabtree, SRA

4.33 out of 5? Only God is perfect. Since this obviously is going to take more time to complete the report (and money is a function of time) fees will have to increase. If the AMC’s insist on continuing to pay “cram down” fees, then all appraisers just need to stop accepting those assignments until they pay C&R per Dodd-Frank. Our profession is “graying” and there are no new appraisers joining the fold. It’s only a mater of time before supply and demand takes over or even worse, Fannie’s CU takes over the appraisal process with the only inspection needed will be by an inspector for $50.

-